Missiles may fall in West Asia, but the shockwaves hit your fuel bill, your savings, and the global economy within hours.

When conflict erupts in West Asia, the immediate images are of airstrikes, damaged infrastructure and rising regional tension. But far from the battlefield, another impact unfolds quietly and swiftly — in stock markets, oil terminals, currency exchanges and government budgets. The latest financial tremors show how a regional war can carve a deep and lasting hole in the global economy.

Markets reacted almost instantly. Equity indices fell sharply, erasing billions in investor wealth within hours. Oil prices surged more than 8 percent in a single session. The Indian rupee slid to 91.47 against the U.S. dollar, reflecting rising global uncertainty and capital outflows. These movements are not isolated financial events. They are early warning signals of broader economic stress.

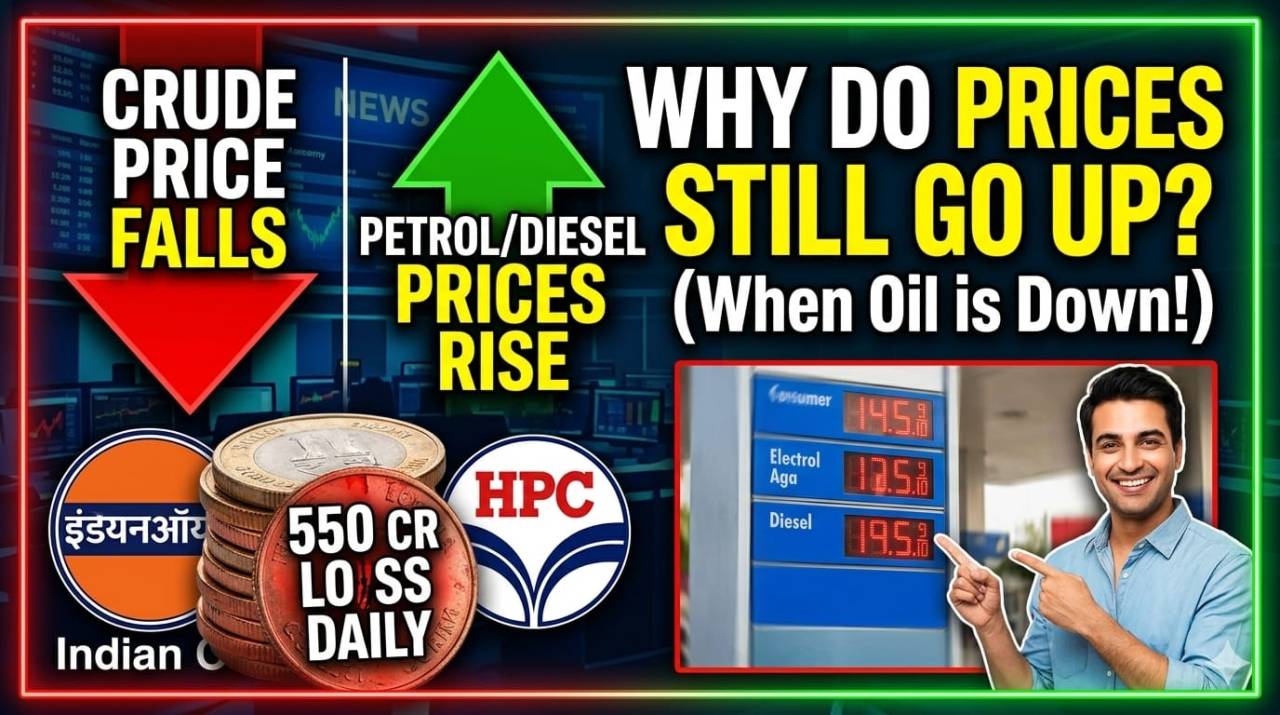

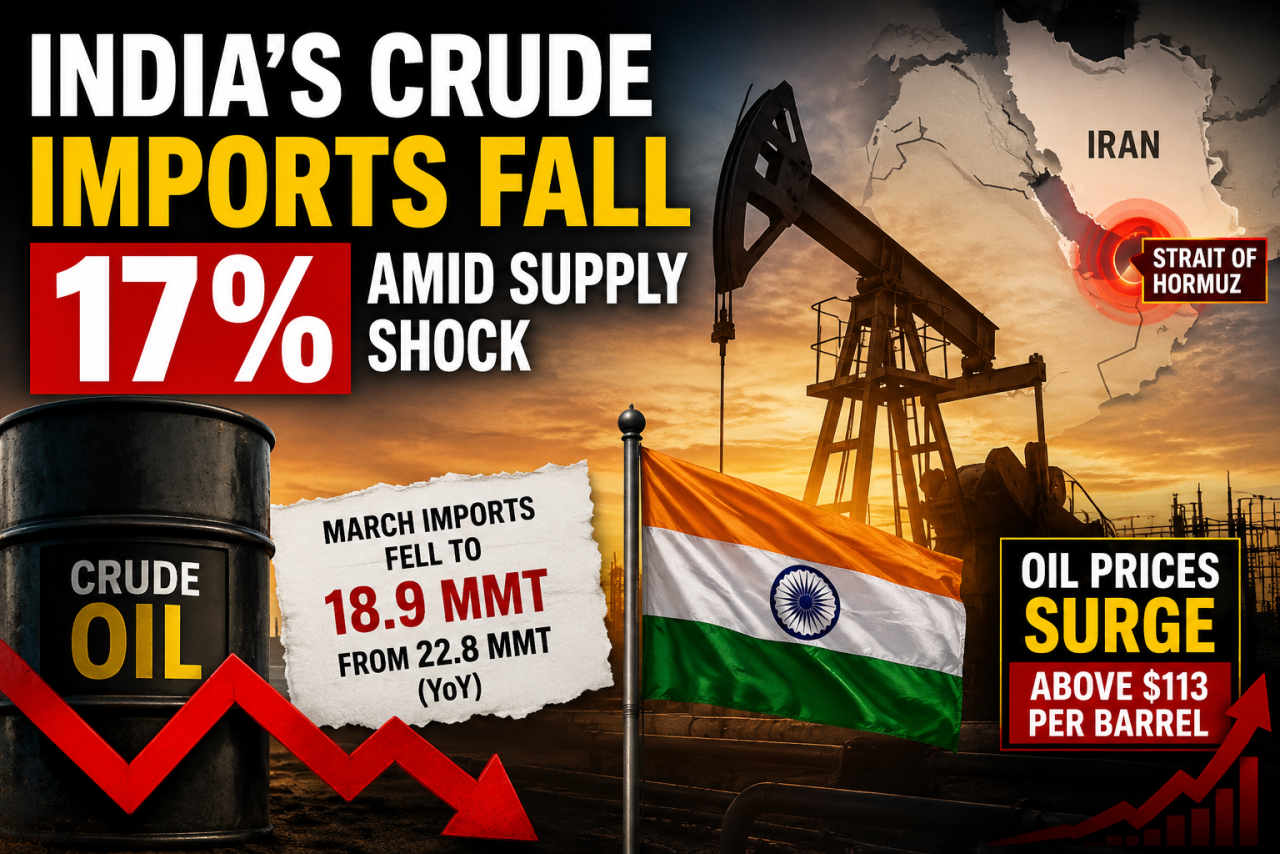

West Asia remains central to the world’s energy supply. Any escalation in the region raises fears about disruptions to oil production or shipping routes. Even the perception of risk can push crude prices higher, as traders factor in potential supply constraints. When Brent crude climbs above $80 per barrel, the consequences are immediate for major importers like India.

Higher oil prices increase transportation costs, raise input expenses for manufacturers and add pressure on electricity generation. These costs ripple across the economy. Food becomes more expensive as logistics costs rise. Airlines face higher aviation turbine fuel prices. Chemical and paint manufacturers see margins shrink. Insurance premiums climb due to heightened geopolitical risk. Inflationary pressure begins to build long before any physical supply disruption occurs.

The currency market amplifies the shock. As tensions escalate, global investors tend to move funds toward perceived safe-haven assets. Emerging markets often experience capital outflows during such periods. A weakening rupee makes imports more expensive, compounding the impact of rising crude prices. The result is a double burden — higher global prices combined with a weaker domestic currency.

For policymakers, this creates a complex challenge. Containing inflation may require tighter monetary conditions, but higher interest rates can slow economic growth. At the same time, governments face pressure to reduce fuel taxes or expand subsidies to shield consumers from rising costs. Either decision strains public finances. If oil prices remain elevated for an extended period, subsidy bills can widen fiscal deficits and limit spending on infrastructure and social programs.

Stock markets, often described as barometers of economic sentiment, reflect this uncertainty. Investors adjust expectations for corporate earnings in sectors sensitive to energy costs. Aviation, logistics, paints and chemicals are among the first to feel the pressure. When markets fall, the wealth effect also comes into play. Households that see the value of their investments decline may reduce discretionary spending, slowing consumption growth.

Trade and supply chains add another layer of vulnerability. West Asia sits along critical maritime and air corridors. Even limited disruptions can force rerouting of cargo and flights, increasing freight and insurance costs. Longer transit times affect inventory cycles and working capital requirements for businesses. Companies respond by building buffers or diversifying supply sources, both of which raise operational expenses.

The global dimension of the crisis becomes clearer when examining interconnected markets. European economies dependent on imported energy face renewed cost pressures. Asian manufacturing hubs that rely on stable shipping routes monitor freight rates closely. Central banks across continents reassess inflation forecasts. A regional conflict begins to shape global monetary and fiscal policy discussions.

Financial volatility also affects long-term investment decisions. Infrastructure projects, cross-border acquisitions and expansion plans are often delayed when geopolitical risk intensifies. Investors prioritize stability and predictability. Persistent uncertainty reduces risk appetite and slows capital formation. Even if the physical conflict remains geographically contained, its economic consequences spread widely through expectations and financial flows.

There is also a social dimension to the economic impact. Rising fuel and food prices disproportionately affect lower-income households. Slower growth can limit job creation. Small businesses operating on thin margins may struggle with higher input costs. Over time, economic stress can translate into political pressure, complicating governance and policy responses.

History shows that oil shocks linked to geopolitical tensions have repeatedly altered global growth trajectories. While markets may stabilize if tensions ease quickly, prolonged instability can entrench higher inflation and weaker currencies. For developing economies striving to maintain fiscal discipline and stable growth, sustained external shocks pose significant risks.

The recent surge in crude prices and the slide in emerging market currencies underscore how tightly the world economy is linked to developments in West Asia. The conflict may be regional in geography, but its economic reach is global. Energy markets react first, financial markets follow, and eventually households feel the impact in everyday expenses.

The broader lesson is that modern warfare carries consequences far beyond immediate military objectives. In an interconnected economic system, disruptions in one strategic region reverberate through trade networks, investment flows and policy frameworks worldwide. Economic stability depends not only on domestic reforms and fiscal prudence but also on geopolitical calm.

The latest developments serve as a reminder that peace is more than a diplomatic aspiration. It is a cornerstone of economic resilience. When conflict disrupts energy supplies and unsettles financial markets, growth forecasts weaken and fiscal pressures mount. The damage may not appear as dramatic as images from the battlefield, but it accumulates steadily in balance sheets, budgets and household expenses.

War in West Asia does not remain confined to its borders. It moves through oil prices, currencies and capital markets, quietly drilling a hole in the global economy that can take years to repair.

Leave a Comment