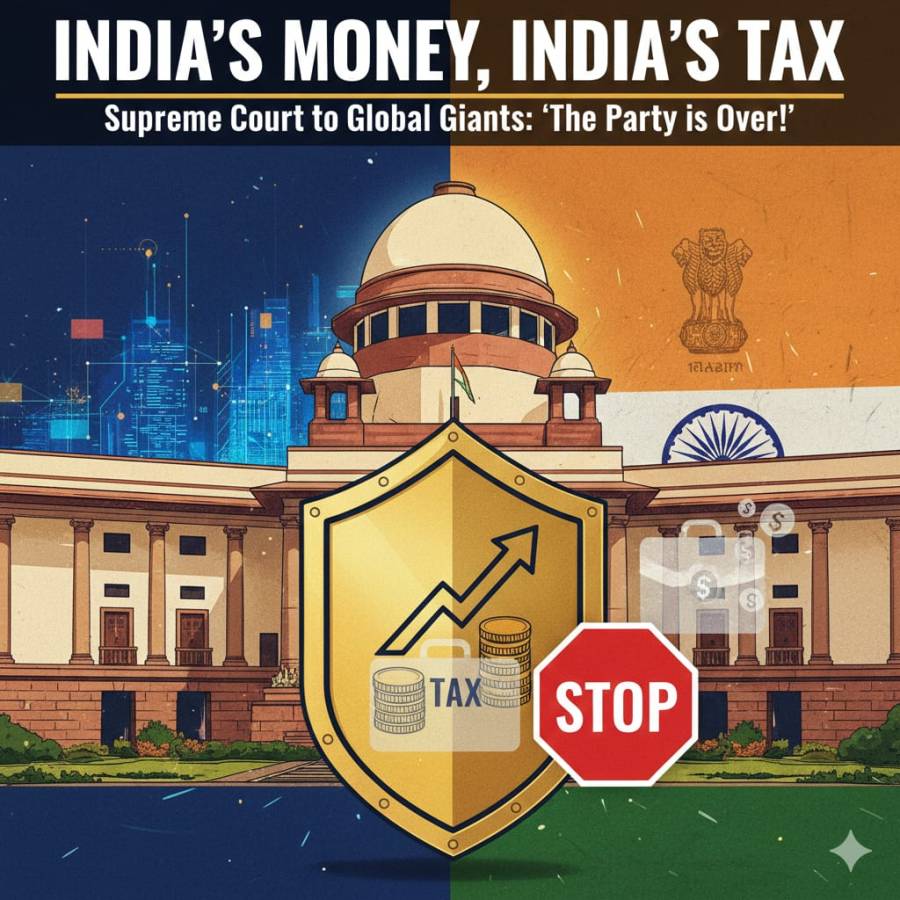

Last week, a quiet but seismic shift happened in the way India does business with the world. You might have seen headlines about "tax sovereignty" or "treaty shopping," but if you strip away the legal jargon, the Supreme Court essentially sent a very clear message to the world’s biggest corporations that India is no longer a place where you can make billions and leave without paying your tab.

The case at the heart of this involves Tiger Global, a massive American investment firm. Back in 2018, when Walmart bought Flipkart, Tiger Global walked away with roughly $1.6 billion (nearly ₹13,000 crore at the time) from selling their shares. But instead of paying taxes in India, they pointed to a piece of paper. Since they had registered their investment through Mauritius, they claimed a decades-old treaty meant India couldn't touch a cent of that profit.

For years, this was the "standard" way of doing business. Big firms would set up tiny "mailbox" offices in tax havens like Mauritius or Singapore, route their Indian investments through them, and bypass the Indian taxman entirely. It was a legal loophole so big you could drive a freight train through it.

The Court’s Reality Check

Justice J.B. Pardiwala and the bench decided it was time for a reality check. In a ruling that felt more like a manifesto for national pride, the court basically said that a tax treaty is a handshake, not a suicide pact.

The judges pointed out something that often gets lost in high-finance talk: when a country loses its power to tax, it loses its independence. If a company earns its wealth from Indian consumers, Indian infrastructure, and Indian workers, then the tax on that profit belongs to the Indian public. To let that money slip away because of a technicality isn't just a loss of revenue—it’s a threat to national security.

The court didn't hold back on the "how." They warned that these loopholes don’t just help companies save money; they open the door for much darker things, like money laundering and "round-tripping," where local wealth is disguised as foreign money to dodge the law.

Why the "Average Joe" Should Care

When the figures run into billions, people tend to lose interest. But the impact is very real. Every time a large multinational avoids a ₹15,000 crore tax bill by using shell companies, that money never reaches the budget for roads, hospitals, or schools. It also creates a deeply unfair playing field. A small shopkeeper in Delhi or a startup founder in Bengaluru has to pay their taxes honestly, while a global giant with a fancy lawyer can just "hop" through a treaty to save billions.

The Supreme Court is now demanding a "checklist" for all future deals. They’ve told the government to stop signing "forever" treaties that don't account for the modern world. In the 1980s, we didn't have a digital economy or billion-dollar app-based companies. The court is saying it’s time to grow up and stop carrying the "legacy of formative years" into 2026.

Final Take

India still wants foreign investment—the court was clear about that. We want the Walmarts and the Tiger Globals of the world to bring their capital here. But the "VIP entrance" that allowed them to skip the tax line is being closed.

From now on, "National Interest" isn't just a slogan; it’s a legal requirement. If you want to profit from the Indian market, you have to contribute to the Indian treasury. It’s a bold, assertive stance that reminds us that while trade is global, sovereignty is local.

Leave a Comment