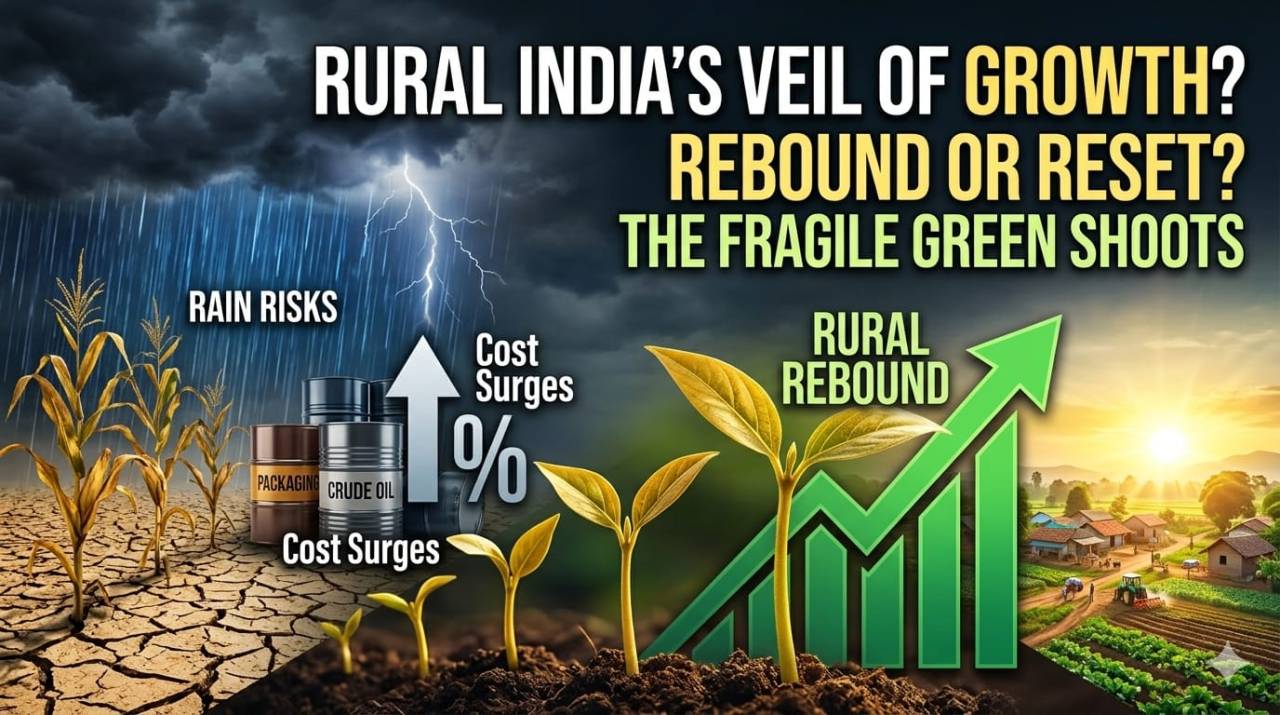

Rural India’s long-awaited consumption revival has finally shown up in the numbers—but just as the rebound gathers pace, rising costs, crude shocks, and an uncertain monsoon are threatening to pull the brakes on the story before it fully takes shape.

The long-awaited revival in India’s rural economy has finally materialized, but its staying power is already being called into question. According to recent financial disclosures for the final quarter of the 2026 fiscal year (Q4FY26), consumer goods and rural-dependent sectors recorded their most robust volume-led recovery in several years. Driven by a temporary sweet spot of cooling inflation, steady agricultural incomes, and an influx of non-farm jobs fueled by state-led infrastructure spending, the rural consumer appeared ready to spend again.

Yet, just as corporate balance sheets began reflecting this vital turnaround, a convergence of macroeconomic headwinds has threatened to cut the celebration short. The nascent recovery in the hinterlands is rapidly running into rising input costs and growing meteorological uncertainty, casting a shadow over the first half of FY27.

The Anatomy of the Rebound

The initial turnaround was a textbook case of favorable economic alignment. Government welfare initiatives and aggressive capital expenditure on infrastructure acted as crucial liquidity lifelines, injecting cash directly into the rural ecosystem. Combined with stable crop prices, this boosted discretionary spending power beyond daily essentials.

A corporate health check underscores this momentum. An analysis of companies within the Nifty Rural Index reveals encouraging metrics for Q4FY26:

- Topline Growth: Net sales rose 11% year-on-year, marking the strongest revenue acceleration in six quarters.

- Profitability Resiliency: Overall profit growth reached 13%, a five-quarter high.

For a brief window, the rural economic engine appeared to be firing on all cylinders, delivering much-needed volume growth to fast-moving consumer goods (FMCG) and industrial players after a prolonged phase of stagnation.

The Cost Crunch and Crude Shock

However, the foundation of this recovery is proving fragile. The primary pressure point is a sharp escalation in global commodity prices, triggered by external geopolitical shocks, including the fallout from tensions in the Middle East earlier in the year.

While many corporations initially cushioned margins using low-cost inventory buffers, that advantage has now largely dissipated. In the current quarter, companies are reporting an immediate double-digit surge in input costs—spanning metals, packaging materials, and logistics.

Crude oil adds another layer of strain. Higher oil prices simultaneously inflate manufacturing and transportation costs while also raising the likelihood of domestic fuel price increases. Historically, such increases act as a direct drain on rural disposable incomes, quickly tightening household budgets.

The Monsoon Gamble

Beyond cost pressures, the most unpredictable variable remains climatic uncertainty. Concerns around an El Niño-driven weak monsoon are clouding the rural outlook. In an economy where a large share of livelihoods remains dependent on agriculture, rainfall variability is not just a production issue—it is a demand shock.

A weak monsoon risks compressing farm incomes while simultaneously reviving food inflation. That combination could erode the very purchasing power that has driven the recent consumption uptick.

Final Take

As corporate India moves deeper into FY27’s early quarters, the optimism of early 2026 is giving way to caution. Analysts expect margin pressure to intensify, forcing companies into a difficult trade-off: absorb rising costs and protect volumes, or pass them on and risk a demand slowdown in rural markets.

Rural India has demonstrated its capacity to rebound. But without stable weather conditions and easing global commodity pressures, this consumption revival risks becoming a short-lived cycle rather than a sustained uptrend.

The long-awaited revival in India’s rural economy has finally materialized, but its staying power is already being called into question. According to recent financial disclosures for the final quarter of the 2026 fiscal year (Q4FY26), consumer goods and rural-dependent sectors recorded their most robust volume-led recovery in several years. Driven by a temporary sweet spot of cooling inflation, steady agricultural incomes, and an influx of non-farm jobs fueled by state-led infrastructure spending, the rural consumer appeared ready to spend again.

Yet, just as corporate balance sheets began reflecting this vital turnaround, a convergence of macroeconomic headwinds has threatened to cut the celebration short. The nascent recovery in the hinterlands is rapidly running into rising input costs and growing meteorological uncertainty, casting a shadow over the first half of FY27.

The Anatomy of the Rebound

The initial turnaround was a textbook case of favorable economic alignment. Government welfare initiatives and aggressive capital expenditure on infrastructure acted as crucial liquidity lifelines, injecting cash directly into the rural ecosystem. Combined with stable crop prices, this boosted discretionary spending power beyond daily essentials.

A corporate health check underscores this momentum. An analysis of companies within the Nifty Rural Index reveals encouraging metrics for Q4FY26:

- Topline Growth: Net sales rose 11% year-on-year, marking the strongest revenue acceleration in six quarters.

- Profitability Resiliency: Overall profit growth reached 13%, a five-quarter high.

For a brief window, the rural economic engine appeared to be firing on all cylinders, delivering much-needed volume growth to fast-moving consumer goods (FMCG) and industrial players after a prolonged phase of stagnation.

The Cost Crunch and Crude Shock

However, the foundation of this recovery is proving fragile. The primary pressure point is a sharp escalation in global commodity prices, triggered by external geopolitical shocks, including the fallout from tensions in the Middle East earlier in the year.

While many corporations initially cushioned margins using low-cost inventory buffers, that advantage has now largely dissipated. In the current quarter, companies are reporting an immediate double-digit surge in input costs—spanning metals, packaging materials, and logistics.

Crude oil adds another layer of strain. Higher oil prices simultaneously inflate manufacturing and transportation costs while also raising the likelihood of domestic fuel price increases. Historically, such increases act as a direct drain on rural disposable incomes, quickly tightening household budgets.

The Monsoon Gamble

Beyond cost pressures, the most unpredictable variable remains climatic uncertainty. Concerns around an El Niño-driven weak monsoon are clouding the rural outlook. In an economy where a large share of livelihoods remains dependent on agriculture, rainfall variability is not just a production issue—it is a demand shock.

A weak monsoon risks compressing farm incomes while simultaneously reviving food inflation. That combination could erode the very purchasing power that has driven the recent consumption uptick.

Final Take

As corporate India moves deeper into FY27’s early quarters, the optimism of early 2026 is giving way to caution. Analysts expect margin pressure to intensify, forcing companies into a difficult trade-off: absorb rising costs and protect volumes, or pass them on and risk a demand slowdown in rural markets.

Rural India has demonstrated its capacity to rebound. But without stable weather conditions and easing global commodity pressures, this consumption revival risks becoming a short-lived cycle rather than a sustained uptrend.

Leave a Comment