Turn your company car into a smart tax-saving tool—car leasing could quietly boost your take-home salary without changing your CTC.

In the evolving landscape of salaried compensation, the idea of a “company car” may sound like a dated executive perk. But beneath the surface, car leasing is quietly re-emerging as one of the most effective and underutilized tools for tax optimization—especially in an era where the new tax regime has stripped away many traditional exemptions.

For today’s professionals, a car lease is no longer just about convenience or status. It is a strategic financial decision that can significantly reduce taxable income and improve take-home salary.

The Mechanics Behind the Tax Advantage

In simple terms, a car lease works as a structured tax shield. Unlike buying a car through a loan—where EMIs are paid from post-tax income—a corporate lease allows the monthly rental to be deducted from your gross salary before tax is calculated.

This simple shift changes everything.

Instead of paying tax on your full salary and then spending on a car, you effectively lower your taxable base first. The result is a smaller tax outgo and higher disposable income without increasing your cost to company (CTC).

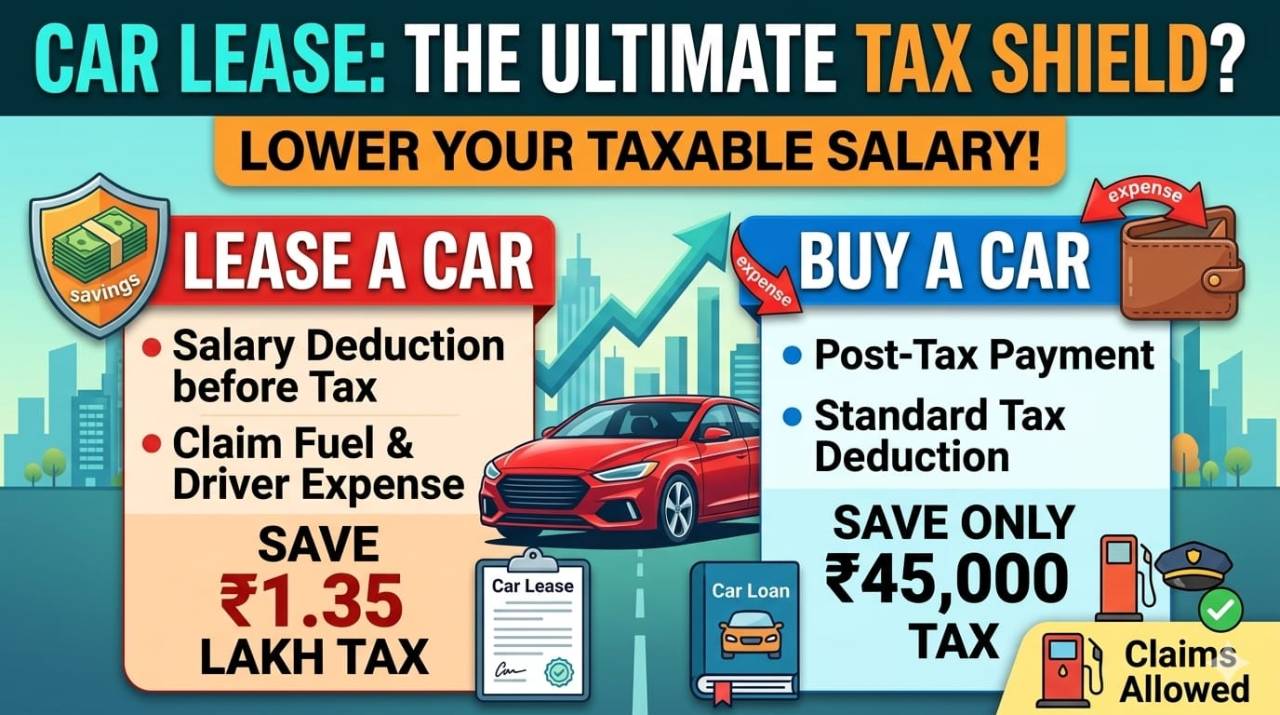

Leasing vs Buying: The Real Difference

The financial contrast between leasing and owning becomes clear when you break down the components.

In a leasing model, expenses such as lease rentals, maintenance, fuel, and even driver salary can be structured as part of your compensation. These are either tax-free or taxed at a significantly lower rate compared to regular salary.

By comparison, when you own a car, most of these expenses are paid from taxed income, with only limited reimbursement benefits.

A typical comparison for a mid-to-senior professional highlights the gap:

- Monthly tax-free component under leasing: ₹45,000

- Monthly tax-free component under ownership: ₹15,000

- Annual tax-free benefit under leasing: ₹5.4 lakh

- Annual tax-free benefit under ownership: ₹1.8 lakh

- Estimated tax saved (30% bracket): ₹1.35 lakh vs ₹45,000

This difference is not marginal—it is structurally significant.

The Perquisite Puzzle, Simplified

One of the biggest concerns around car leasing is the concept of perquisite tax. When a company provides a car for both official and personal use, the benefit is partially taxable.

However, the key lies in how this value is calculated.

The tax department does not assess the actual expense incurred. Instead, it assigns a fixed notional value based on engine capacity:

- Small cars (up to 1.6L engine): low, fixed monthly taxable value

- Larger cars (above 1.6L): slightly higher, but still standardized

In most cases, this taxable value ranges between ₹2,400 and ₹3,300 per month—far lower than the actual cost of maintaining and running a vehicle.

This gap between real expense and notional taxation is where the true tax efficiency of leasing emerges.

Beyond Tax: The Lifestyle Shift

The appeal of car leasing goes beyond numbers. It aligns with a broader shift toward a usage-based economy, where access matters more than ownership.

Leasing eliminates the need for a large upfront payment, allowing professionals to keep their capital invested elsewhere—potentially earning better returns in equities, mutual funds, or other assets.

It also simplifies life. Maintenance, insurance, servicing, and roadside assistance are typically bundled into the lease, reducing both financial unpredictability and administrative hassle.

Then there is flexibility. At the end of the lease term, usually three to five years, you can upgrade to a newer model without worrying about depreciation or resale value.

A Strategic Opportunity in a Restricted Tax Environment

As the new tax regime continues to narrow deduction avenues, car leasing stands out as one of the few remaining “white” strategies to optimize taxes within the system.

It is no longer limited to senior executives. Increasingly, mid-level professionals with structured compensation packages are leveraging it to reshape their salary in a more tax-efficient way.

Final Take

Now, car leasing is a financial lever.

When structured correctly, it allows you to convert a portion of your taxable salary into a lower-taxed or tax-efficient benefit, without compromising on lifestyle or mobility.

In a time when every percentage point of tax saved matters, ignoring this option could mean leaving money on the table.

If your organization offers a car lease policy, it may be time to look at it differently—not as an expense, but as a smart and legal way to increase your take-home income while driving the car you want.

In the evolving landscape of salaried compensation, the idea of a “company car” may sound like a dated executive perk. But beneath the surface, car leasing is quietly re-emerging as one of the most effective and underutilized tools for tax optimization—especially in an era where the new tax regime has stripped away many traditional exemptions.

For today’s professionals, a car lease is no longer just about convenience or status. It is a strategic financial decision that can significantly reduce taxable income and improve take-home salary.

The Mechanics Behind the Tax Advantage

In simple terms, a car lease works as a structured tax shield. Unlike buying a car through a loan—where EMIs are paid from post-tax income—a corporate lease allows the monthly rental to be deducted from your gross salary before tax is calculated.

This simple shift changes everything.

Instead of paying tax on your full salary and then spending on a car, you effectively lower your taxable base first. The result is a smaller tax outgo and higher disposable income without increasing your cost to company (CTC).

Leasing vs Buying: The Real Difference

The financial contrast between leasing and owning becomes clear when you break down the components.

In a leasing model, expenses such as lease rentals, maintenance, fuel, and even driver salary can be structured as part of your compensation. These are either tax-free or taxed at a significantly lower rate compared to regular salary.

By comparison, when you own a car, most of these expenses are paid from taxed income, with only limited reimbursement benefits.

A typical comparison for a mid-to-senior professional highlights the gap:

- Monthly tax-free component under leasing: ₹45,000

- Monthly tax-free component under ownership: ₹15,000

- Annual tax-free benefit under leasing: ₹5.4 lakh

- Annual tax-free benefit under ownership: ₹1.8 lakh

- Estimated tax saved (30% bracket): ₹1.35 lakh vs ₹45,000

This difference is not marginal—it is structurally significant.

The Perquisite Puzzle, Simplified

One of the biggest concerns around car leasing is the concept of perquisite tax. When a company provides a car for both official and personal use, the benefit is partially taxable.

However, the key lies in how this value is calculated.

The tax department does not assess the actual expense incurred. Instead, it assigns a fixed notional value based on engine capacity:

- Small cars (up to 1.6L engine): low, fixed monthly taxable value

- Larger cars (above 1.6L): slightly higher, but still standardized

In most cases, this taxable value ranges between ₹2,400 and ₹3,300 per month—far lower than the actual cost of maintaining and running a vehicle.

This gap between real expense and notional taxation is where the true tax efficiency of leasing emerges.

Beyond Tax: The Lifestyle Shift

The appeal of car leasing goes beyond numbers. It aligns with a broader shift toward a usage-based economy, where access matters more than ownership.

Leasing eliminates the need for a large upfront payment, allowing professionals to keep their capital invested elsewhere—potentially earning better returns in equities, mutual funds, or other assets.

It also simplifies life. Maintenance, insurance, servicing, and roadside assistance are typically bundled into the lease, reducing both financial unpredictability and administrative hassle.

Then there is flexibility. At the end of the lease term, usually three to five years, you can upgrade to a newer model without worrying about depreciation or resale value.

A Strategic Opportunity in a Restricted Tax Environment

As the new tax regime continues to narrow deduction avenues, car leasing stands out as one of the few remaining “white” strategies to optimize taxes within the system.

It is no longer limited to senior executives. Increasingly, mid-level professionals with structured compensation packages are leveraging it to reshape their salary in a more tax-efficient way.

Final Take

Now, car leasing is a financial lever.

When structured correctly, it allows you to convert a portion of your taxable salary into a lower-taxed or tax-efficient benefit, without compromising on lifestyle or mobility.

In a time when every percentage point of tax saved matters, ignoring this option could mean leaving money on the table.

If your organization offers a car lease policy, it may be time to look at it differently—not as an expense, but as a smart and legal way to increase your take-home income while driving the car you want.

Leave a Comment